On This Page

Overview

What are long-term disability (LTD) benefits?

What is my LTD claim worth?

What injuries qualify for LTD?

Denied or terminated LTD benefits? Your legal options

How do injury lawyers help with LTD claims?

What are the settlement options for LTD claims?

Hear from our clients

Frequently Asked Questions

Talk to Our Long Term Disability Lawyers

Overview

In 2022, 27% of Canadians aged 15 years and older reported they had one or more disabilities that limited them in their daily activities, up from 22% in 2017, according to the Canadian Survey on Disability from Statistics Canada. Part of this increase was attributed to a rise in mental health-related disabilities.

Navigating life with functional impairments, managing insurance companies, recovery, and the possibility of returning to work, can feel overwhelming. Seeking legal advice early is one way people making a long-term disability claim can ensure they receive the compensation they are entitled to.

Talk to Our Long Term Disability Lawyers

On This Page

Overview

What are long-term disability (LTD) benefits?

What is my LTD claim worth?

What injuries qualify for LTD?

Denied or terminated LTD benefits? Your legal options

How do injury lawyers help with LTD claims?

What are the settlement options for LTD claims?

Hear from our clients

Frequently Asked Questions

What are long-term disability (LTD) benefits?

Long Term Disability (LTD) benefits are monthly payments you receive from an insurance company when you are unable to work for medical reasons, typically provided as a group insurance plan through your employer or union. You can also buy individual Long Term Disability policies from a broker if you are self-employed or not covered by a group insurance policy through your employer.

Common LTD Issues We Handle:

Denied Claims

When LTD insurers deny payments to a person who has applied, often claiming there is not enough evidence to support that you cannot work.

Terminated Benefits

When the LTD insurer terminates benefits for a person who has already been receiving LTD benefits.

"Own” vs "Any” Occupation Disputes

Many policies provide "own occupation" coverage for the first two years and after that you must be disabled from "any occupation."

Chronic Pain & Mental Health Claims

Some disabling conditions cannot be proven through objective evidence like x-rays or CT scans. Chronic pain and psychological diagnoses are often reliant on subjective reporting.

Recovery Plan Compliance

Issues arising when insurance companies claim you haven't followed recommended treatment plans.

Social Media Impact

When insurance companies use your social media posts against your claim.

Subrogation Issues

When you're receiving LTD benefits and also pursuing a personal injury claim from an accident.

What is my LTD claim worth?

Our LTD benefits calculator gives you an estimate based on your income, policy terms, and possible offsets. Use it as a starting point to understand what your benefits might look like.

Factors that affect your LTD benefits include:

-

The age to which benefits are payable (commonly to age 65, but varies by policy)

-

The amount of your monthly LTD benefit (usually a percentage of your income)

-

The definition of "Total Disability" in your specific policy

-

Offsets such as Canada Pension Plan Disability or Workers' Compensation benefits

Calculate My Long Term Disability Claim Worth.

Use our calculator to estimate your potential claim.

What injuries qualify for LTD?

Common injuries and conditions that can qualify include:

Musculoskeletal Injuries

Back injuries, joint damage, and repetitive strain injuries.

Neurological Disorders

Multiple sclerosis, Parkinson’s disease, or traumatic brain injuries.

Mental Health Conditions

Depression, anxiety, PTSD, and some other psychiatric disorders.

Cardiovascular Conditions

Heart disease or stroke-related complications that restrict physical activity.

Chronic Pain Syndromes

Fibromyalgia, CRPS, and other conditions causing persistent pain.

Cancer & Treatment-Related Effects

Surgery, chemotherapy, or radiation side effects that interfere with work.

Is your injury not listed above? You might still be entitled to compensation. LTD benefits are not limited to a specific list of injuries or conditions. Instead, eligibility depends on whether a medical condition prevents you from working according to your policy’s definition of disability. Our legal experts can help.

Denied or terminated LTD benefits? Your legal options

If your LTD benefits have been denied or terminated you have two options, each with their own timeline.

Internal Appeal

You can appeal the decision internally by writing to the LTD insurer and going through their internal appeals process. The denial letter from your insurance company will set out the specific deadline for filing an appeal.

Lawsuit

The second option is to sue your LTD insurer for breach of contract. If you pursue a lawsuit against your insurer, you typically have two years to file your claim.

Alberta Limitation Period

Deadlines play a critical role in long-term disability disputes. Missing them could mean losing your right to appeal or sue. The general limitation period in Alberta is two years. However, there can be exceptions. For this reason, it is important to consult with a lawyer following a denial or termination of disability benefits to ensure your right to pursue one of these options is protected.

Learn more about time-limits on long-term disability claims through our resources, or by reading Alberta’s Limitations Act.

There are advantages and disadvantages to appealing internally versus suing your LTD insurer. These considerations are specific to your individual circumstances and would best be evaluated in consultation with a lawyer.

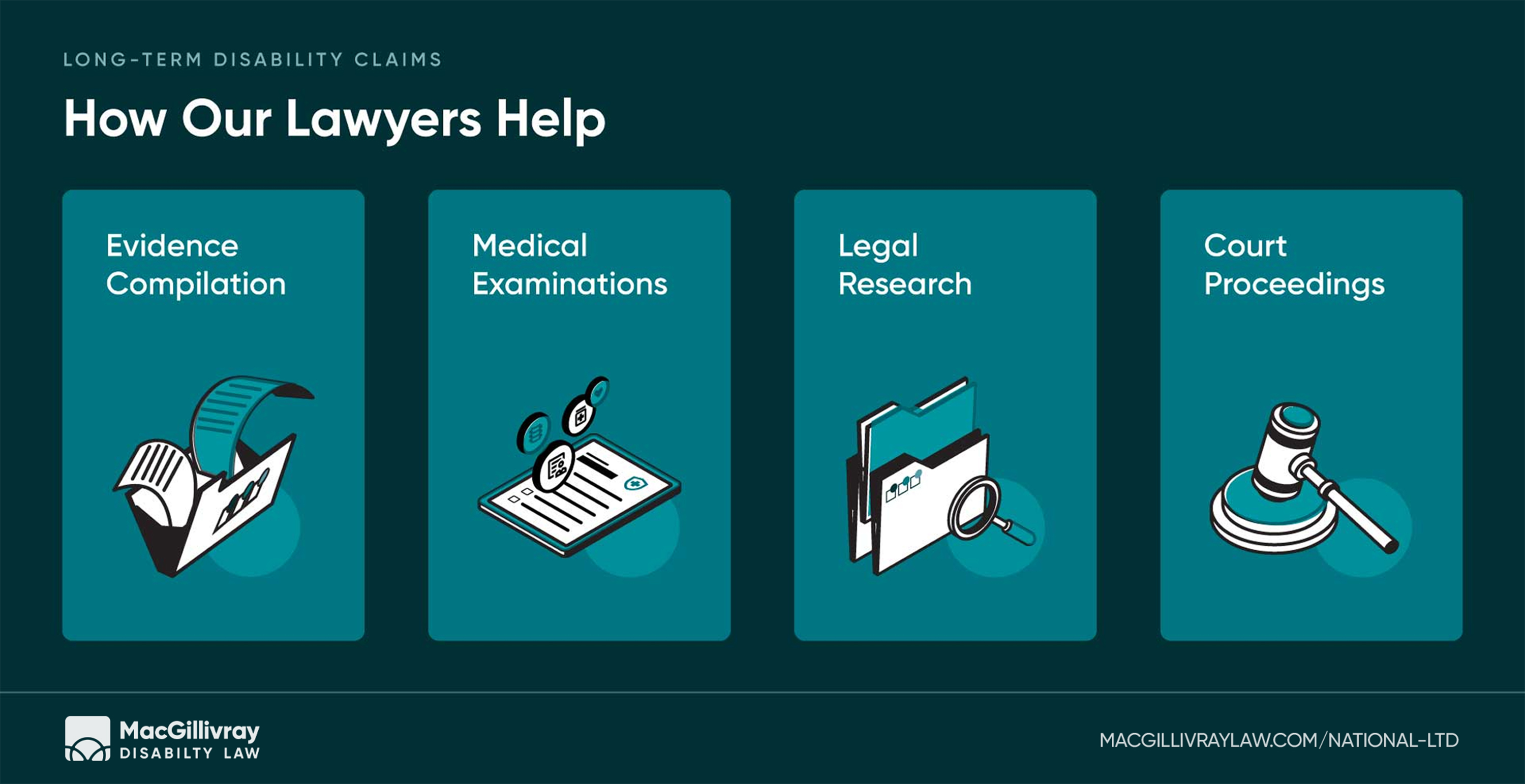

How do injury lawyers help with LTD claims?

LTD insurers sometimes deny payments to people who have applied or terminate benefits for those who are already receiving them. These decisions are often based on the insurer’s opinion that there is insufficient evidence showing that you cannot work. Insurers frequently rely on assessments from their own medical teams to justify denials or terminations.

Some disabling conditions, such as chronic pain or psychological diagnoses, cannot always be proven through “objective” medical evidence like x-rays or CT scans. Because of this, LTD claims often rely on detailed, subjective medical documentation.

An experienced lawyer knows how to gather and present the strongest possible evidence in these cases, ensuring that your claim clearly demonstrates the impact of your disability.

Evidence Compilation

We know the right questions to ask your doctors and other healthcare providers to compile the best evidence in support of your disability claim. By collecting comprehensive records and reports, we help build a claim that accurately reflects your condition and work limitations.

Medical Examinations

When additional evaluation is needed, we refer clients to trusted specialists for Independent Medical Examinations. These expert assessments provide objective support for your claim and can be critical when insurers challenge the severity or impact of your disability.

Legal Research

Disability insurance policies can be complex and full of technical language. We conduct thorough legal research to interpret your policy, identify your rights, and understand how similar cases have been handled in court. This ensures your claim is supported by a sound legal strategy.

Court Proceedings

If a fair resolution cannot be reached through negotiation or appeal, we guide your case through the court process. Our lawyers manage deadlines, file the necessary documents, and advocate on your behalf to move the case toward resolution. We work to make the process as clear and manageable as possible while pursuing the benefits you are entitled to.

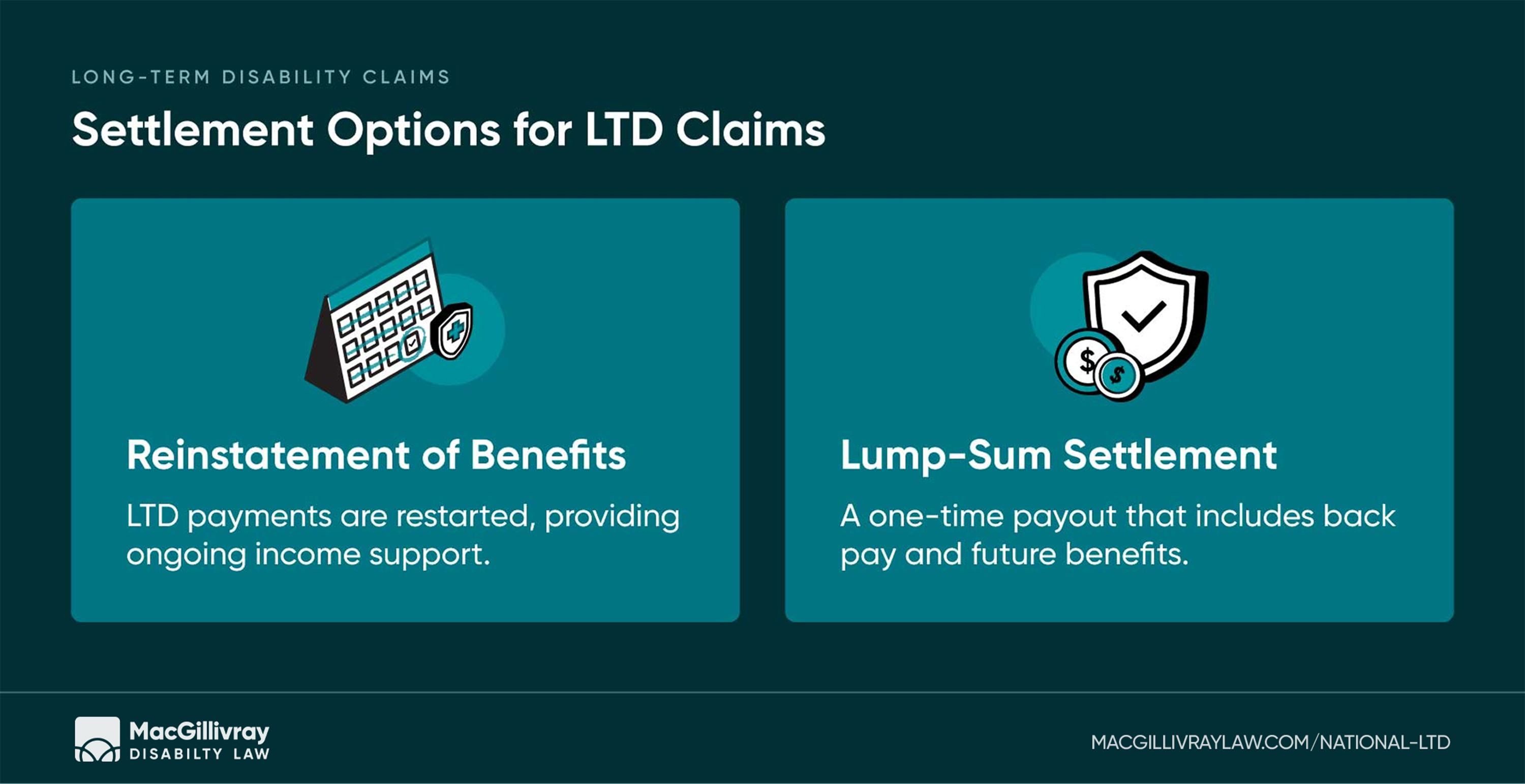

What are the settlement options for LTD claims?

A settlement is an agreement between you and your insurance company to resolve your long-term disability (LTD) claim. Below are the most common LTD settlement options and important deadlines to be aware of.

Reinstatement of Benefits

Reinstatement means your regular benefit payments resume after they have been stopped. This option allows you to continue receiving monthly LTD payments under your policy, providing ongoing financial support.

Lump-Sum Settlement

In some cases, you may be offered a one-time payment that represents the total value of your insurance policy. This typically includes:

- Back benefits you should have already received

- Future disability payments estimated over the life of your claim

A lump sum provides immediate financial relief and permanently closes your claim. However, because you cannot return to the insurer for more benefits, it is important to work with a lawyer to ensure the amount offered is fair.

Hear from our clients

I spent 30 years being gaslit and dismissed by most medical professionals. Having dealt with so many who brushed me off, Steve’s compassion and understanding were a welcome reprieve from that negativity. He made me feel heard and seen, and he empathized with my situation on a deeper level than many of these so-called “medical professionals” ever did. I will always remember it. Thank you ❤️

Kathy Conway

4 months ago

After fighting for my rights I turned to MacGillivray law for help. My life was no longer my own. Years of fighting, debt and physical pain took a toll on me and my family. MacGillivray Law took on the fight. They gave me my life back! No more looking over my shoulder. No more worry. No more stress. I owe MacGillivray Law more than they will ever know. Thank you for giving us our future back! Our gratitude is endless!

Trevor Berringer

5 months ago

They are more than just lawyers. They didn't just handle my claim; they provided a lifeline, working tirelessly as if they were helping a broken person get back on their feet. Thanks to their professional and unwavering support, I was finally able to focus on my recovery. I am so grateful for their guidance and advocacy. They are more than just lawyers; they are truly compassionate advocates.

Sabiha Shahid

6 months ago

Frequently Asked Questions

You can always apply for CPPD benefits. If approved for both, you can draw from both sources, but CPPD benefits might be subtracted from your LTD policy benefits through a process called ‘offsetting.’

Yes, if you have been denied LTD benefits, a lump sum settlement may be available. This represents the total of your insurance policy, including back benefits and future disability payments.

If you do not participate in recommended recovery programs, your insurance company might stop your benefits. It’s important to follow medical advice, and if you disagree with recommendations, get a second opinion.

Yes, insurance companies can access your social media posts and use them against you. It’s important not to post content that contradicts your disability claims.

“Own occupation” means you cannot perform the duties of your specific job. “Any occupation” means you cannot perform duties of any job you’re reasonably suited for by education, training, or experience.

- Closure and certainty

- Tax advantages (future benefits portion is not taxable)

- Freedom to return to work without reporting to insurance company

- Security for your family

Your LTD insurer might be entitled to a portion of any settlement you receive through a process called ‘subrogation.’ We can help coordinate between your LTD claim and personal injury case.